Differences between IFRS and US GAAP

The world allows two major frameworks for accounting in the whole world today. The General Accepted Accounting Principles and the International Financial Reporting Standards are the two major frameworks. The two frameworks have been constituted to create a harmony for accounting procedures globally. The GAAP methodology is the main accounting framework used in the US while the IFRS is the accounting framework that is majorly accepted internationally. The two frameworks have been tailored to allow the provision of fair accounting grounds to the users. However, there are major differences that can be seen from the two frameworks. Discussed herein is a list of key differences that define the two accounting frameworks.

Definition of Terms

International Financial Reporting Standards (IFRS), is a set of standards for accounting that are developed by an independent nonprofit organization known as the International Accounting Standards Board whereas the Generally Accepted Accounting Principles (GAAP), are a set of principles, criteria, and processes in accounting that should be followed by a company in the process of compiling their financial statements.

IFRS serves to provide a worldwide framework that shows how companies should prepare and disclose their financial statements. The IFRS guides the process of preparing the financial statements but does not dictate how the reporting should be specifically done. GAAP combines authoritative principles set by policy boards, and acceptable ways of recording and reporting monetary data.

The reason IFRS exists is to try and harmonize the standards with a view to simplifying the whole process of accounting. The guidelines given by the IFRS enables a company to use one style of reporting all through the accounts reporting (1). The single standards also enable investors and auditors to have a more direct view of finances without the small differences caused by different reporting styles.

The main function of the GAAP is to ensure the least amount of inconsistency in the financial reports of a company to enable easy analysis and evaluation of information by investors. GAAP is also important in facilitating the comparison of financial data among different business entities.

Key Notable Differences between US GAAP and IFRS

Principle and Rule

The single and most notable difference between GAAP and IFRS is that GAAP is based on rules while IFRS is based on principles. This difference can attribute to a major potential in different interpretations of similar transactions. This can cause a major and extensive disclosure in financial statements.

Consolidation Models

The consolidation models for the IFRS entails the focus on control, without considering the form of the entity that has invested. An investor can control the business when they have the right to variable returns from the business and are capable of influencing the returns due to their power over the business investee (2). Control, in this case, means that the investor has: power over the investee, rights to variable returns with the investee, and the ability to exercise their control over the investee to affect the returns going to them.

On the other hand, there are two models for consolidation in the US GAAP.in the first model, entities are exposed to the influence of variable interest entity (VIE). If the VIE model cannot be applied, then the entities are subjected to the voting interest model (VIM). The VIE model allows a reporting entity to have control of the financial interests in a VIE (2). Under the VIM, interest in controlling the financial processes of the reporting entity is existent if the reporting entity has an interest in another entity.

Income Statement

IFRS does not allow for the segregation of items while GAAP shows the items right below the net income.

Both the IFRS and the US GAAP necessitates a prominent presentation of an income statement as a primary statement. Both systems present the financial statement in different formats.

The IFRS has no format that is prescribed when preparing an income statement. The entity should find the method which shall be used in presenting the expenses, either by function or nature (3). By nature, additional disclosure of expenses is required if a functional presentation is used. The IFRS requires that an income statement must include:

- Method

- Loss or gain after taxing attributed to the results and the recalibration of the discontinued operations.

- Finance costs

- Expenses of tax

- Periodical loss or profit

- Shared results, for associates and joint ventures which used the equity, after tax.

On the other hand, the US GAAP presents their income statements in two ways.

- Single step format.

This format factors in all expenses and classifies them by function. The expenses, in this case, are deducted from the total income to outline the income before tax.

- Multiple – step format.

This is where the expense of sales is deducted from the sales to show the gross profit. Other income and expenses are also outlined in order to give the income before tax. Regulations of the SEC require that the registrants should categorize their expenses by function.

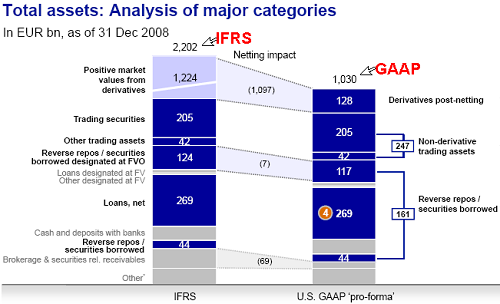

Asset Valuation

Asset valuation differences are attributed to the difference in the indicators of impairment, the unit of accounting assets, the measurement of impairment, and the eventual recovery of assets that were impaired. The IFRS does not allow the use of LIFO methodology of costing while the US GAAP allows the use of LIFO costing methodology (4). The implication herein is that a company which adopts the IFRS and uses the LIFO method under US GAAP will be forced to switch to a methodology that enables allowable costing.

Recognition of Revenue

In recognition of revenues, there may be key differences in the way business entities operate. There could be different ways that the entities handle their products and services in the marketplace.

The IFRS puts into play two standards that primarily capture transactions of revenue in either of four major categories.

- Selling of commodities and goods

- Provision of services

- Contracts in construction

- Use of the entity’s assets by others

The criteria that are used take into consideration that there is a considerable chance of reliably measuring how the benefits associated with the transaction will trickle to the entity.

On the other hand, there is an extensive guide for recognizing revenue in GAAP framework. The guidance employs a lot of literature that is provided by setters of standards (4). The guidance generally provides that revenue can either be realized or earned.

Methodology

Different methods are used to evaluate the accounting treatment. GAAP focuses more on the kind of literature that is used while the IFRS is keener on the pattern used to review the facts.

IFRS provides a platform for the pursuit of a singular model of financial reporting while the US GAAP allows a high risk and reward model.

Inventory Valuation

IFRS allows LIFO to be used while GAAP allows the flexibility of either choosing LIFO or FIFO

Per Share Earnings. In the IFRS consideration, individual interim period calculations are not averaged in the earning- per- share calculation (4). The consideration given is that IFRS can only allow the calculation of earnings per share from continuing operations and net income. The entity should, therefore, make use of the same method of recording inventory and there is no use of any discretion in picking out any applicable method.

On the other hand, GAAP allows the period incremental shares to be averaged in the computation. This means that GAAP will allow the earnings per share to be calculated for operations that are continual, discontinued operations, and net income. For the US GAAP, after the inventory is sold, there is the allowance of either using the LIFO or FIFO method. The flexibility allows the entity to use their judgment to choose the method which best applies to their inventories.

Conclusion

The IFRS and US GAAP frameworks both have their own advantages and disadvantages. While the two entities help to assess the accounting world on various capacities, notable differences prove as strengths and weaknesses of the systems. The convergence of the two frameworks could enhance the process and results of accounting.

Summary of key differences between IFRS and US GAAP

| Factor | IFRS | US GAAP

|

| 1. Asset Valuation | Assets can be re-evaluated upwards when an active market is existent for what is abstract. It also allows the PP and E to be revalued to a more fair value. | Assets can only be written down but cannot be written up. The PP and E use history cost for valuation. |

| 2. Principle and rule | IFRS provides principles that should be followed by the best judgment of the entity. | GAAP specifies the practices involved as rules to prevent opportunistic measures by entities on maximizing profits. |

| 3. Inventory Valuation | Only permits LIFO or the average weighted cost and LIFO is not permitted (4).

Inventory is carried at the lower cost or the market. |

Permits both LIFO and FIFO, weighted average cost. Inventory is carried at the lower cost or net value that is realizable. |

| 4. Revenue recognition | There are no clear specifications about how revenue should be measured or timed (4). | Provisional guidance is very specific on what revenue is and how it should be measured. |

| 5. Development costs | Certain costs can be taken advantage of and repaid over multiple periods. | Can be charged to expenses as they have been sustained |

- Difference between Traditional Commerce and Ecommerce - February 16, 2018

- The Differences between Copay and Deductible - February 6, 2018

- Differences between Personal Property and Real Property - January 29, 2018

Search DifferenceBetween.net :

1 Comment

Leave a Response

References :

[0]Shamrock, S. (2012). IFRS and US GAAP(1st ed., pp. 5-8). Hoboken, N.J.: John Wiley.

[1]http://rsmus.com/pdf/consolidations-at-a-glance.pdf

[2]http://accounting-financial-tax.com/2008/06/ifrs-vs-gaap-balance-sheet-and-income-statement/

[3]https://www.pwc.com/us/en/cfodirect/assets/pdf/accounting-guides/pwc-ifrs-us-gaap-similarities-and-differences-2016.pdf

[4]https://www.flickr.com/photos/pmagsa/3476195168/

Its good information