Difference Between Exemption and Deduction

Deduction and exemption are provisions adopted in taxation with the purpose of decreasing the overall tax liability for specific individuals.

What is Exemption?

Exemption refers to the situation where the income of an individual is not subjected to the standard taxation method hence not charged.

The sole purpose of the exemption is to reduce the tax liability of a specific individual who satisfies certain criteria.

For example, an individual may reduce his or her tax burden through exemption where he or she requests tax exemption due to the number of a dependent.

What is Deduction?

Deductions refer to the amount that is not subjected to taxation. For example, individuals are required to subtract the amount, which is not subject to taxation, which includes expenses and relief.

Standardized deductions deduct a standardized amount that is set out by the tax body. This amount varies from one country to another and usually depends on whether one is married, single, and widowed.

Itemized deductions allow an individual to lower his or her tax liability by including specific items for tax deductions following particular qualification criteria.

Difference Between Exemption and Deduction

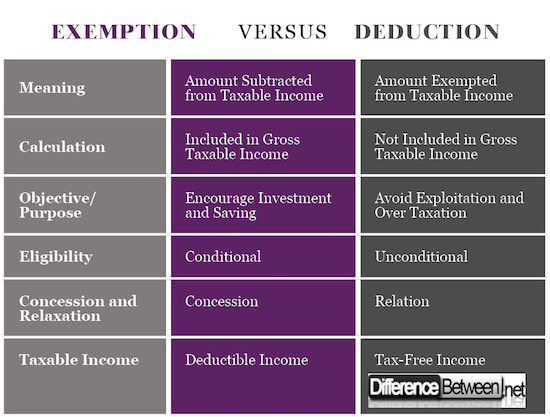

1) Meaning of Exemption and Deduction

Deduction refers to subtraction of the amount that is not subjected to taxation. Some of the amounts that are deducted must meet specific qualifications that are laid down by the taxation body.

The amount deducted include tax relief, tax rebates, amounts used to cater for dependents, and amount used to cater for health services or social security schemes.

Exemption refers to the amount excluded from taxation. Certain income is exempted from tax and will not contribute to the total revenue of an individual

2) Calculation for Exemption and Deduction

The method through which deductions and exemptions are calculated can help an individual to understand the difference.

In the calculation of deductions, the entire amount that has qualified for deductions is added to the gross taxable income after which it is later deducted before the total amount is subjected to the tax scale.

However, not all the amount and income that qualify for exemptions from part of the gross taxable income. Exemptions are deducted before the total taxable income is realized.

3) Objective/Purpose of Exemption and Deduction

Deductions are introduced in taxation as a method of encouraging individuals to save and invest a sizeable proportion of their income. Individuals who have invested much of their income in certain instruments lower their taxable income.

On the other hand, the purpose of introducing exemptions is to ensure that the disadvantaged section of the society is not overtaxed.

Countries have a single taxation method, which taxes rich and low-income people uniformly. To eradicate this form of discrimination, exemptions are introduced to the low-income population to prevent exploitation.

4) Eligibility for Exemption and Deduction

A deduction is a conditional criterion that is accessible to only those people who meet specific qualifications that are provided by the taxation body.

Individuals willing to qualify for deductions are encouraged to save a specific proportion of their income or invest their earnings in particular areas, which may include manufacturing and infrastructure development.

Exemptions are an unconditional relief that is afforded to the people in the bottom social class in the society to prevent over taxation while at the same time allowing them to have higher purchasing power and meet their social needs.

5) Concession and Relaxation of Exemption and Deduction

Tax deductions are a concession, which requires individuals or companies not to pay taxes that would otherwise be owed to the tax authority as an inducement to invest.

Governments use tax concessions as a competitive strategy of allowing foreigners to invest in their country.

Exemptions fall under tax relaxation, which ensures that a specific amount is not subjected to taxable income hence relieving the tax burden to low-income groups.

6) Taxable Income for Exemption and Deduction

The deduction only applies to deductible income. This means that all the profits, which are subject to deductions that include life insurance, medical insurance, and donations to charitable institutions are available.

Moreover, deductions will only be allowed to specific persons that qualify the particular criteria.

On the other hand, exemptions are only applicable only where tax-free income is eligible for tax exemption. On the other hand, an exemption is granted to all the persons.

Difference Between Exemption and Deduction

Summary of of Exemption and Deduction

- Deduction and exemption are provisions used in taxation to reduce the tax burden on individuals who are usually exposed to high taxation levels.

- One of the main difference between deduction and exemption is that deduction refers to the subtraction of the qualified amount that is not subjected to taxation while exemption applies to the relief offered to the low-income earners where they are not subjected to tax.

- Other differences between deduction and exemption aspects include objectives, effects on taxable income, a method of calculation, eligibility for deduction and exemption, concession, and the relation among others.

- Difference Between Gross NPA and Net NPA - April 20, 2018

- Difference Between Job Description and Job Specification - April 13, 2018

- Difference Between Yoga and Power Yoga - April 10, 2018

Search DifferenceBetween.net :

Leave a Response

References :

[0]Givord, Pauline, Roland Rathelot, and Patrick Sillard. "Place-based tax exemptions and displacement effects: An evaluation of the Zones Franches Urbaines program." Regional Science and Urban Economics 43.1 (2013): 151-163.

[1]Givord, Pauline, Roland Rathelot, and Patrick Sillard. "Place-based tax exemptions and displacement effects: An evaluation of the Zones Franches Urbaines program." Regional Science and Urban Economics 43.1 (2013): 151-163.

[2]King, Mervyn A., and Don Fullerton. The taxation of income from capital: a comparative studyof the United States, the United Kingdom, Sweden and West Germany. University of Chicago Press, 2010.

[3]Kullgren, Jeffrey T., et al. "Health care use and decision making among lower-income families in high-deductible health plans." Archives of internal medicine 170.21 (2010): 1918-1925.

[4]Image credit: https://www.flickr.com/photos/investmentzen/28374128013

[5]Image credit: https://www.flickr.com/photos/aidanmorgan/5524891107